Redfin Says It’s the Best Time to Buy a Home Since Mid-September: Should You Buy Now or Hold On?

Thanks to a record number of price cuts and a big improvement in mortgage rates, home buying conditions have improved tremendously.

Taken together, you might be able to snag a lower purchase price and finance the property with a mortgage rate about .50% lower than what was on offer last month.

Does this mean it’s time to rush out to buy a home? Or does it continue to pay to be patient?

Personally, I’m still in the no-rush camp, but if you do see something you love, the price tag could be a little lower.

And there may be less competition as it tends to drop off later in the year as buyers get consumed with other things.

Unseasonal Increase in For-Sale Listings as Asking Prices Drop

Redfin reported this morning that some “glimmers of hope” are emerging for prospective home buyers.

The first one being that new listings increased 1.5% from a year ago during the four weeks ending November 5th.

This was just the second such increase since July 2022, a testament to the continued short supply plaguing the housing market.

They noted that this increase is partly because new listings were falling during this period last year.

At the same time, active listings are at their highest level since the beginning of 2023, and months of supply ticked up 0.2 points to 3.6 months.

Inventory remains constrained nationally, with 4 to 5 months typically signifying healthy supply. But it is rising, which appears to be leading to price reductions.

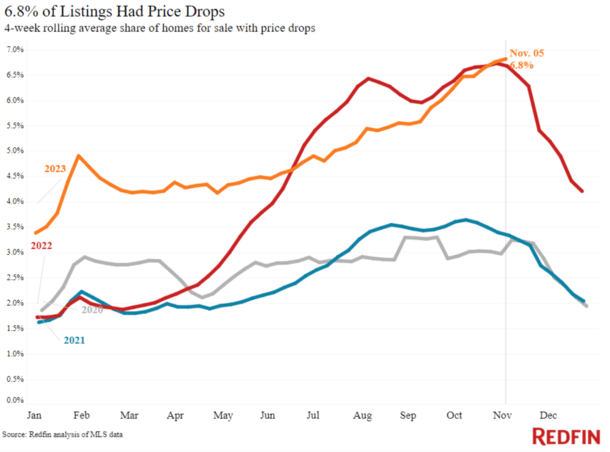

And the share of listed homes with a price drop increased to 6.8%, a new record high.

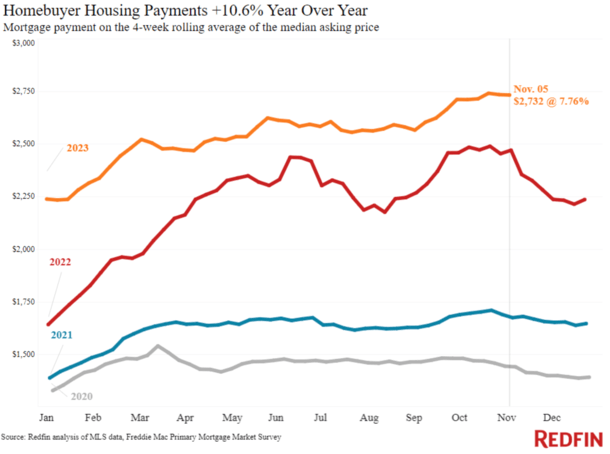

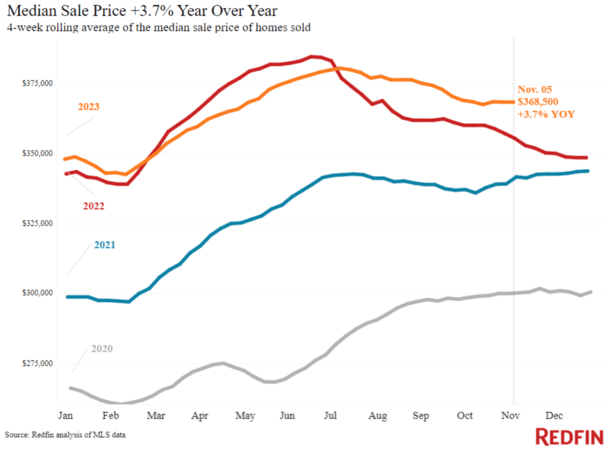

However, the median asking price was still 4.9% higher than a year ago at $379,725, the biggest increase in over a year.

This means the median monthly mortgage payment remains near an all-time high of $2,732, assuming a 7.76% 30-year fixed mortgage rate.

The monthly mortgage payment hit an all-time high two weeks ago when it was $8 higher.

Total Housing Payments Are Up Over 10% From a Year Ago

When you factor in the steeper asking prices and the higher mortgage rates, total housing payments are still up 10.6% year-over-year.

So despite increased inventory and rising price cuts, it’s not as if discounts are rolling in.

The only real improvement has been a pullback in rates, providing a boost to affordability in an otherwise bleak environment.

If you zoom out and look at all of 2023, and ignore the month of October, mortgage rates remain close to their highs for the year.

In other words, while affordability improved relative to a month ago, it remains at/near its worst levels of the year.

As such, it might benefit buyers to continue to wait for prices/rates to come down further.

This counters advice from Redfin economists, who “recommend that serious homebuyers consider locking in a mortgage now.”

The economists, like many others, are cautious with regard to mortgage rates and concerned they could easily reverse course.

They cite the upcoming CPI report, which will be released on November 14th. If you reveals that inflation ticked up again, mortgage rates could resume their climb.

And they’re not wrong that it’s much easier for mortgage rates to go up than come down.

Mortgage lenders are generally defensive in their pricing. They’re happy to raise rates at the drop of a hat, but reluctant to lower them, even if the data supports it.

So if you are far along in the home buying process, it could make sense to lock in a mortgage rate and avoid taking chances.

Prices and Rates Could Continue to Fall into December

It could make sense to continue to wait to buy a home, as pressure has finally seemed to ease on mortgage rates.

At the same time, housing inventory is climbing at a time of year when it typically doesn’t, indicating possible incoming weakness on pricing.

This means it could be beneficial to bide your time on a home purchase, instead of rushing in to nab what could in hindsight be a small discount relative to recent levels.

A while back, I dug through Freddie Mac data and found that mortgage rates tend to be lowest in December.

The 30-year fixed has averaged 5.97% in the month of December, nearly 0.25% lower than the 6.18% rate typically seen in the months of April and May.

Those months also tend to be when homes sell for the most money as it’s the traditional spring home buying season.

There are more buyers out, more demand, increased bidding wars and competition, and higher rates.

So there’s certainly an argument to be made about buying a home in the latter months of 2023, at least relative to other months recently.

But overall, it still feels like it’s not a good time to buy a home, at least from an investment standpoint, in most areas of the country.

Until asking prices and mortgage rates come down, it could pay to continue waiting for better.

Comments are closed.