What Do Mortgage Underwriters Do? Decide If You’re Approved!

Here’s

some

Q&A

with

regard

to

the

home

loan

approval

process:

“What

do

underwriters

do?”

Once

you

actually

apply

for

a

home

loan,

your

mortgage

application

will

be

organized

by

a

loan

processor

and

then

sent

along

to

a

loan

underwriter,

who

will

determine

if

you

qualify

for

a

mortgage.

The

underwriter

can

be

your

best

friend

or

your

worst

enemy,

so

it’s

important

to

put

your

best

foot

forward.

The

expression,

“you’ve

only

got

one

chance

to

make

a

first

impression”

comes

to

mind

here.

Trust

me,

you’ll

want

to

get

it

right

the

first

time

to

avoid

going

down

the

bureaucratic

rabbit

hole.

The

Underwriter

Will

Approve,

Suspend,

or

Decline

Your

Mortgage

Application

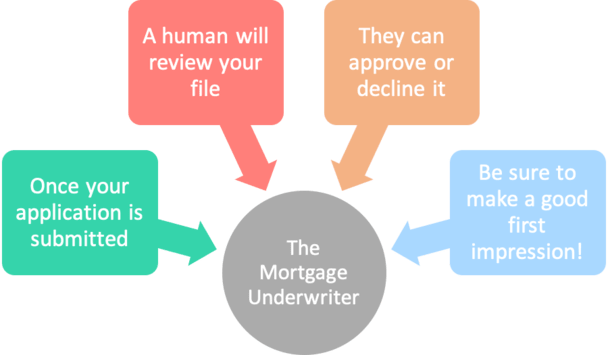

-

After

you

formally

apply

for

a

home

loan

your

file

will

be

submitted

to

the

underwriting

department -

A

human

underwriter

will

then

review

your

loan

application

and

decision

it -

Their

job

is

to

approve,

suspend,

or

decline

your

application

based

on

its

contents -

It’s

paramount

to

submit

a

clean

file

to

boost

your

chances

of

loan

approval

Simply

put,

the

loan

underwriter’s

job

is

to

approve,

suspend,

or

decline

your

mortgage

application.

If

the

loan

is

approved,

you’ll

receive

a

list

of

“conditions”

which

must

be

met

before

you

receive

your

loan

documents.

So

in

essence,

it’s

really

a

conditional

loan

approval.

If

the

loan

is

suspended,

you’ll

need

to

supply

additional

information

or

loan

documentation

to

move

it

to

approved

conditional

status.

If

the

loan

is

declined,

you’ll

more

than

likely

need

to

apply

elsewhere

with

another

bank

or

mortgage

lender,

or

take

steps

to

fix

whatever

went

wrong.

The

Three

C’s

of

Mortgage

Underwriting

-

Credit

–

payment

behavior

over

time

(your

credit

report) -

Capacity

–

ability

to

repay

the

home

loan

(your

income

and

assets) -

Collateral

–

value

of

the

underlying

asset

(the

property)

Now

you

may

be

wondering

how

underwriters

determine

the

outcome

of

your

mortgage

application?

Well,

there

are

the

“three

C’s

of

underwriting,”

otherwise

known

as

credit

reputation,

capacity,

and

collateral.

Credit

reputation

has

to

do

with

your

credit

history,

including

past

foreclosures,

bankruptcies,

judgments,

and

basically

measures

your

willingness

to

pay

your

debts.

[What

credit

score

do

I

need

to

get

a

mortgage?]

If

you’ve

had

previous

mortgage

delinquencies

or

even

non-housing

related

delinquencies,

these

will

need

to

be

taken

into

account.

Typically

these

items

will

be

reflected

in

your

three-digit

credit

score,

which

can

actually

eliminate

you

from

contention

without

any

further

underwriting

necessary

if

you

fall

below

a

certain

threshold.

For

example,

you

need

a

620

FICO

for

a

conforming

loan

and

at

least

a

500

score

for

an

FHA

loan.

Your

history

supporting

significant

amounts

of

debt

is

also

important;

if

the

most

you’ve

ever

financed

has

been

a

plasma

TV,

the

underwriter

may

think

twice

about

approving

your

six-figure

loan

application.

Capacity

deals

with

a

borrower’s

ability

to

repay

a

loan,

using

things

like

debt-to-income

ratio,

employment

history,

salary,

cash

reserves,

loan

program

and

more.

In

short,

the

underwriter

wants

to

know

that

you

can

pay

back

the

mortgage

you’re

applying

for

before

granting

approval.

[How

much

house

can

I

afford?]

Finally,

collateral

involves

the

borrower’s

down

payment,

loan-to-value

ratio,

property

type,

and

property

use,

as

the

lender

will

be

stuck

with

the

home

if

the

borrower

fails

to

make

timely

mortgage

payments.

A

home

appraisal

will

be

ordered

to

determine

the

value

of

the

property

using

an

independent

appraiser.

Mortgage

Underwriters

Consider

Layered

Risk

-

They

don’t

just

look

at

one

aspect

of

your

borrower

profile

in

a

vacuum -

They

consider

all

factors

together

to

make

a

sound

underwriting

decision -

Those

with

risk

in

one

area

who

are

able

to

compensate

for

it

may

be

approved -

While

those

with

issues

in

all

areas

might

be

denied

due

to

layered

risk

Now

it’s

important

to

understand

that

the

three

C’s

are

not

independent

of

one

another.

All

three

must

be

considered

simultaneously

to

understand

the

level

of

“layered

risk”

that

could

be

present

in

said

loan

application.

For

example,

if

the

borrower

has

a

less-than-stellar

credit

score,

limited

asset

reserves,

and

a

minimal

down

payment,

the

risk

layering

could

be

deemed

excessive,

leading

to

denial.

Consider

a

home

buyer

with

zero

down

payment,

a

600

FICO

score,

and

only

$1,000

in

the

bank,

who

just

started

a

new

job.

Conversely,

consider

a

home

buyer

putting

down

20%,

with

a

760

FICO

score

and

$50,000

in

cash

reserves,

who

has

worked

the

same

job

for

a

decade.

Obviously

the

second

borrower

sounds

like

a

much

better

candidate

for

a

mortgage.

This

is

the

underwriter’s

discretion,

and

can

certainly

be

subjective

based

on

other

factors

such

as

their

occupation,

how

long

the

borrower

has

been

in

the

line

of

work,

why

the

credit

score

is

less

than

perfect,

and

so

on.

The

underwriter

must

decide,

based

on

all

the

criteria,

if

the

borrower

is

an

acceptable

risk

for

the

mortgage

lender,

and

if

the

end

product

can

be

resold

without

difficulty

to

investors.

Layered

risk

is

a

major

reason

why

the

mortgage

crisis

got

so

out

of

hand.

Countless

borrowers

applied

for

mortgages

with

stated

income

and

zero

down

financing,

which

is

certainly

very

high

risk,

and

were

easily

approved.

Rising

home

prices

covered

up

the

mess

for

a

while,

but

it

didn’t

take

long

for

everything

to

unravel.

This

is

why

sound

mortgage

underwriting

is

so

critical

to

a

healthy

housing

market.

What

Shouldn’t

You

Do

During

Underwriting?

One

last

thing.

When

the

underwriter

is

working

to

decision

your

loan

file,

you

as

the

borrower

should

do

your

part

as

well.

This

means

NOT

applying

for

new

lines

of

credit,

such

as

a

credit

card

or

a

new

auto

loan.

And

not

making

large

purchases.

If

you

do,

they

could

show

up

on

the

credit

report

or

be

reflected

in

your

credit

scores.

The

last

thing

you

want

is

a

lower

credit

score

to

jeopardize

your

loan

application.

The

same

goes

for

moving

assets

around

from

one

bank

account

to

another,

or

switching

jobs.

It

might

sound

crazy,

but

just

about

anything

you

can

think

of

has

happened.

Long

story

short,

you

want

to

remain

in

a

holding

pattern

while

your

loan

goes

through

underwriting

and

ideally

gets

funded.

Once

the

loan

is

funded

and

recorded,

you

can

go

on

about

your

business,

whether

it’s

buying

new

furniture

or

applying

for

a

new

credit

card.

But

until

that

time,

you

can

make

life

easier

for

everyone

(including

yourself)

by

doing

nothing!

Mortgage

Underwriter

FAQ

Do

underwriters

work

for

the

bank/lender?

Yes,

underwriters

are

employees

of

banks,

lenders,

and

mortgage

bankers.

They

work

on

the

operational

side

of

things,

making

loan

decisions

after

the

sales

team

brings

the

loan

in

the

door.

This

means

they

work

in

the

same

building

as

the

sales

team.

How

long

does

underwriting

take?

It

might

only

take

an

underwriter

a

few

hours

to

comb

through

a

loan

file

and

approve,

suspend,

or

deny

it.

However,

mortgage

lenders

only

have

so

many

underwriters

available,

and

surely

the

number

of

loans

in

the

pipeline

will

exceed

the

number

of

staff.

As

such,

much

of

the

time

might

be

waiting

in

the

queue

until

a

pair

of

eyeballs

actually

look

over

your

loan.

So

if

you’re

wondering

how

quickly

can

underwriting

be

done,

it

may

depend

on

how

busy

the

company

is

and

if

there’s

any

backlog.

Once

your

file

does

get

in

front

of

an

underwriter,

the

average

time

for

underwriting

is

pretty

quick,

often

24

hours

or

less.

Why

do

underwriters

take

so

long?

Hmm…I

don’t

know,

because

they’re

approving

a

six-figure

loan

amount,

or

seven,

to

a

complete

stranger.

As

noted,

the

actual

underwriting

might

not

take

that

long,

but

the

amount

of

available

underwriters

(humans)

might

be

low.

So

you

could

just

be

in

the

queue.

A

clean

loan

file

will

get

approved

faster

and

with

fewer

conditions

so

get

it

right

before

the

underwriter

even

sees

it.

Do

underwriters

verify

employment?

While

employment

is

generally

verified

nowadays

when

you

take

out

a

mortgage,

it

might

not

be

the

underwriter

verifying

it.

Instead,

the

loan

processor

may

obtain

the

verification

of

employment

(VOE).

Many

use

the

“The

Work

Number,”

an

independent

third-party

employment

verification

company

now

owned

by

credit

bureau

Equifax.

How

much

do

loan

underwriters

make?

They

can

make

pretty

good

money.

Salaries

may

be

in

the

high

five

figures

to

low

six

figures

if

they’re

seasoned

and

skilled

in

underwriting

all

types

of

loans,

including

FHA,

VA,

and

so

on.

If

you

start

as

a

junior

underwriter

the

salary

could

be

less

than

$50,000.

But

once

you

become

a

senior

loan

underwriter,

the

pay

can

jump

up

tremendously.

It

may

also

be

possible

to

earn

overtime.

Do

underwriters

make

commission?

They

shouldn’t

because

that

would

be

a

conflict

of

interest.

They

should

approve/deny

loans

based

on

the

characteristics

of

the

loan

file,

not

because

they

need

to

hit

a

certain

number.

Compensating

them

for

loan

quality

might

be

a

different

story,

but

again

could

lead

to

discrimination

if

they

cherrypick

only

the

best

loans.

Do

underwriters

work

weekends?

I’ve

heard

of

some

that

have.

I

don’t

know

if

they

do

on

a

regular

basis,

but

if

loan

volume

picks

up

in

a

short

period

of

time

it’s

possible

to

come

in

on

a

Saturday

or

Sunday.

The

mortgage

world

is

all

about

highs

and

lows,

so

sometimes

it

might

be

slow

and

other

times

it’s

impossible

to

keep

up.

Are

underwriters

warm

and

friendly?

They

can

be

if

you

don’t

rub

them

the

wrong

way.

I

look

at

mortgages

kind

of

like

the

DMV.

Show

up

with

the

right

paperwork

and

a

good

attitude

and

you’ll

get

in

and

out

before

you

know

it.

Do

the

opposite

at

your

peril!

(photo:

Joelk75)

Comments are closed.