Portfolio Lenders: A Solution for Hard to Close Mortgages

If

you’re

having

trouble

obtaining

a

home

loan,

perhaps

after

speaking

to

multiple

banks,

lenders

and

even

a

mortgage

broker,

consider

reaching

out

to

a

“portfolio

lender.”

Simply

put,

portfolio

lenders

keep

the

loans

they

originate

(instead

of

selling

them

off

to

investors),

which

gives

them

added

flexibility

when

it

comes

to

underwriting

guidelines.

As

such,

they

might

be

able

to

offer

unique

solutions

others

cannot,

or

they

could

have

a

special

loan

program

not

found

elsewhere.

For

example,

a

portfolio

lender

may

be

willing

to

originate

a

no-down

payment

mortgage

while

others

are

only

able

to

provide

a

loan

up

to

97%

loan-to-value

(LTV).

Or

they

could

be

more

forgiving

when

it

comes

to

marginal

credit,

a

high

DTI

ratio,

limited

documentation,

or

any

other

number

of

issues

that

could

block

you

from

obtaining

a

mortgage

via

traditional

channels.

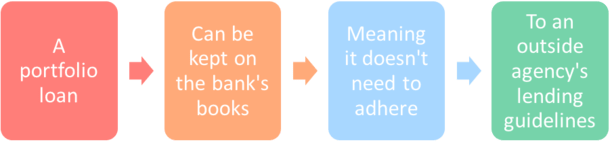

What

Is

a

Portfolio

Loan?

-

A

home

loan

kept

on

the

bank’s

books

as

opposed

to

being

sold

off

to

investors -

May

come

with

special

terms

or

features

that

other

banks/lenders

don’t

offer -

Such

as

no

down

payment

requirement,

an

interest-only

feature,

or

a

unique

loan

term -

Can

also

be

useful

for

borrowers

with

hard-to-close

loans

who

may

have

been

denied

elsewhere

In

short,

a

“portfolio

loan”

is

one

that

is

kept

in

the

bank

or

mortgage

lender’s

portfolio,

meaning

it

isn’t

sold

off

on

the

secondary

market

shortly

after

origination.

This

allows

these

lenders

to

take

on

greater

amounts

of

risk,

or

finance

loans

that

are

outside

the

traditional

“credit

box”

because

they

don’t

need

to

adhere

to

specific

underwriting

criteria.

Nowadays,

most

home

loans

are

backed

by

Fannie

Mae

or

Freddie

Mac,

collectively

known

as

the

government-sponsored

enterprises

(GSEs).

Or

they’re

government

loans

backed

by

the

FHA,

USDA,

or

VA.

All

of

these

agencies

have

very

specific

underwriting

standards

that

must

be

met,

whether

it’s

a

minimum

FICO

score

of

620

for

a

conforming

loan.

Or

a

minimum

down

payment

of

3.5%

for

an

FHA

loan.

If

these

conditions

aren’t

met,

the

loans

can’t

be

packaged

as

agency

mortgage-backed

securities

(MBS)

and

delivered

and

sold.

Since

small

and

mid-sized

lenders

often

don’t

have

the

capacity

to

keep

the

loans

they

fund,

they

must

ensure

the

mortgages

they

underwrite

meet

these

criteria.

As

a

result,

you

have

a

lot

of

lenders

making

plain,

vanilla

loans

that

you

could

get

just

about

anywhere.

The

only

real

difference

might

be

pricing

and

service.

On

the

other

hand,

portfolio

lenders

who

aren’t

beholden

to

anyone

have

the

ability

to

make

up

their

own

rules

and

offer

unique

loan

programs

as

they

see

fit.

After

all,

they’re

keeping

the

loans

and

taking

the

risk,

so

they

don’t

need

to

answer

to

a

third

party

agency

or

investor.

This

means

they

can

offer

home

loans

to

borrowers

with

500

FICO

scores,

loans

without

traditional

documentation,

or

utilize

underwriting

based

on

rents

(DSCR

loans).

Ultimately,

they

can

create

their

own

lending

menu

based

on

their

very

own

risk

appetite.

Portfolio

Loans

Can

Solve

Your

Financing

Problem

-

Large

loan

amount -

High

DTI

ratio -

Low

credit

score -

Recent

credit

event

such

as

short

sale

or

foreclosure -

Late

mortgage

payment -

Owner

of

multiple

investment

properties -

Asset-based

qualification -

Limited

or

uneven

employment

history -

Qualifying

via

subject

property’s

rental

income -

Unique

loan

program

not

offered

elsewhere

such

as

an

ARM,

interest-only,

zero

down,

etc.

There

are

a

variety

of

reasons

why

you

might

want/need

a

portfolio

loan.

But

it’s

generally

going

to

be

when

your

loan

doesn’t

fit

the

guidelines

of

the

GSEs

(Fannie/Freddie)

or

Ginnie

Mae,

which

supports

the

FHA

and

VA

loan

programs.

As

noted,

these

types

of

mortgage

lenders

can

offer

things

the

competition

can’t

because

they’re

willing

to

keep

the

loans

on

their

books,

instead

of

relying

on

an

investor

to

buy

the

loans

shortly

after

origination.

This

allows

them

to

offer

mortgages

that

fall

outside

the

guidelines

of

Fannie

Mae,

Freddie

Mac,

the

FHA,

the

VA,

and

the

USDA.

That’s

why

you

might

hear

that

a

friend

or

family

member

was

able

to

get

their

mortgage

refinanced

with

Bank

X

despite

having

a

low

credit

score

or

a

high LTV.

Or

that

a

borrower

was

able

to

get

a

$5

million

jumbo

loan,

an

interest-only

mortgage,

or

something

else

that

might

be

considered

out-of-reach.

Perhaps

even

an

ultra-low

mortgage

rate!

A

portfolio

loan

could

also

be

helpful

if

you’ve

experienced

a

recent

credit

event,

such

as

a

late

mortgage

payment,

a

short

sale,

or

a

foreclosure.

Or

if

you

have

limited

documentation,

think

a

stated

income

loan

or

a

DSCR

loan

if

you’re

an

investor.

Really,

anything

that

falls

outside

the

box

might

be

considered

by

one

of

these

lenders.

Who

Offers

Portfolio

Loans?

Some

of

the

largest

portfolio

lenders

include

Chase,

U.S.

Bank,

and

Wells

Fargo,

but

there

are

smaller

players

out

there

as

well.

Before

they

failed,

First

Republic

Bank

offered

special

portfolio

mortgages

to

high-net-worth

clients

that

couldn’t

be

found

elsewhere.

They

came

with

below-market

interest

rates,

interest-only

periods,

and

other

special

features.

Ironically,

this

is

what

caused

them

to

go

under.

Their

loans

were

basically

too

good

to

be

true.

It’s

also

possible

to

find

a

portfolio

loan

with

a

local

credit

union

as

they

tend

to

keep

more

of

the

loans

they

originate.

For

example,

many

of

them

offer

100%

financing,

adjustable-rate

mortgages,

and

home

equity

lines

of

credit,

while

a

typical

nonbank

lender

may

not

offer

any

of

those

things.

Generally,

portfolio

lenders

are

depositories

because

they

need

a

lot

of

capital

to

fund

and

hold

the

loans

after

origination.

But

there

are

also

non-QM

lenders

out

there

that

offer

similar

products,

which

may

not

actually

be

held

in

portfolio

because

they

have

their

own

non-agency

investors

as

well.

Portfolio

Loan

Interest

Rates

Can

Vary

Tremendously

-

Portfolio

mortgage

rates

may

be

higher

than

rates

found

with

other

lenders

if

the

loan

program

in

question

isn’t

available

elsewhere -

This

means

you

may

pay

for

the

added

flexibility

if

they’re

the

only

company

offering

what

you

need -

Or

they

could

be

below-market

special

deals

for

customers

with

a

lot

of

assets -

Either

way

still

take

the

time

to

shop

around

as

you

would

any

other

type

of

loan

Now

let’s

talk

about

portfolio

loan

mortgage

rates,

which

can

vary

widely

just

like

any

other

type

of

mortgage

rate.

Ultimately,

many

mortgages

originated

today

are

commodities

because

they

tend

to

fit

the

same

underwriting

guidelines

of

an

outside

agency

like

Fannie,

Freddie,

or

the

FHA.

As

such,

the

differentiating

factor

is

often

interest

rate

and

closing

costs,

since

they’re

all

basically

selling

the

same

thing.

The

only

real

difference

aside

from

that

might

be

customer

service,

or

in

the

case

of

a

company

like

Rocket

Mortgage,

a

quirky

ad

campaign

and

some

unique

technology.

For

portfolio

lenders

who

offer

a

truly

unique

product,

loan

pricing

is

entirely

up

to

them,

within

what

is

reasonable.

This

means

rates

can

exhibit

a

wide

range.

If

the

loan

program

is

higher-risk

and

only

offered

by

them,

expect

rates

significantly

higher

than

what

a

typical

market

rate

might

be.

But

if

their

portfolio

home

loan

program

is

just

slightly

more

flexible

than

what

the

agencies

mentioned

above

allow,

mortgage

rates

may

be

comparable

or

just

a

bit

higher.

It’s

also

possible

for

the

rate

offered

to

be

even

more

competitive,

or

below-market,

assuming

you

have

a

relationship

with

the

bank

in

question.

It

really

depends

on

your

particular

loan

scenario,

how

risky

it

is,

if

others

lenders

offer

similar

financing,

and

so

on.

At

the

end

of

the

day,

if

the

loan

you

need

isn’t

offered

by

other

banks,

you

should

go

into

it

expecting

a

higher

rate.

But

if

you

can

get

the

deal

done,

it

might

be

a

win

regardless.

Who

Actually

Owns

My

Home

Loan?

-

Most

home

loans

are

sold

to

another

company

shortly

after

origination -

This

means

the

bank

that

funded

your

loan

likely

won’t

service

it

(collect

monthly

payments) -

Look

out

for

paperwork

from

a

new

loan

servicing

company

after

your

loan

funds -

The

exception

is

a

portfolio

loan,

which

may

be

held

and

serviced

by

the

originating

lender

for

the

life

of

the

loan

Many

mortgages

today

are

originated

by

one

entity,

such

as

a

mortgage

broker

or

a

direct

lender,

then

quickly

resold

to

investors

who

earn

money

from

the

repayment

of

the

loan

over

time.

Gone

are

the

days

of

the

neighborhood

bank

offering

you

a

mortgage

and

expecting

you

to

repay

it

over

30

years,

culminating

in

you

walking

down

to

the

branch

with

your

final

payment

in

hand.

Well,

there

might

be

some,

but

it’s

now

the

exception

rather

than

the

rule.

In

fact,

this

is

part

of

the

reason

why

the

mortgage

crisis

took

place

in

the

early

2000s.

Because

originators

no

longer

kept

the

home

loans

they

made,

they

were

happy

to

take

on

more

risk.

After

all,

if

they

weren’t

the

ones

holding

the

loans,

it

didn’t

matter

how

they

performed,

so

long

as

they

were

underwritten

based

on

acceptable

standards.

They

received

their

commission

for

closing

the

loan,

not

based

on

loan

performance.

Today,

you’d

be

lucky

to

have

your

originating

bank

hold

your

mortgage

for

more

than

a

month.

And

this

can

be

frustrating,

especially

when

determining

where

to

send

your

first

mortgage

payment.

Or

when

attempting

to

do

your

taxes

and

receiving

multiple

form

1098s.

This

is

why

you

have

to

be

especially

careful

when

you

purchase

a

home

with

a

mortgage

or

refinance

your

existing

mortgage.

The

last

thing

you’ll

want

to

do

is

miss

a

monthly

payment

right

off

the

bat.

So

keep

an

eye

out

for

a

loan

ownership

change

form

in

the

mail

shortly

after

your

mortgage

closes.

If

your

loan

is

sold,

it

will

spell

out

the

new

loan

servicer’s

contact

information,

as

well

as

when

your

first

payment

to

them

is

due.

Comments are closed.